MEMBERS-ONLY FACT SHEET

Departing Load Charges

Last Updated February 11, 2025

Departing load charges are an assessment of non-bypassable charges on load that is not served by the utilities. CALSSA opposes these charges because they discourage clean energy and have questionable legal justification. As we explore options to challenge these charges, however, we produce this fact sheet with our current understanding of how they are assessed.

Non-export projects are becoming more common for several reasons.

Non-export projects are exempt from the public works requirements of AB 2143.

NEM1 and NEM2 customers can expand their existing systems and maintain NEM status on the existing capacity if the new capacity is managed separately as non-export.

Interconnection delays can be avoided by not exporting to the grid.

The NEM and NBT tariffs include exemptions from departing load charges. This exemption has not been the subject of much attention, but it is a valuable benefit of NEM/NBT. Non-export is not NEM/NBT, so these charges have come into play.

Because assessing departing load charges on a large number of solar customers is new, the utilities do not have clear and consistent guidelines. This fact sheet represents CALSSA’s understanding of what the utilities are currently doing. We look forward to input from members as the utilities standardize their practices. We will keep this fact sheet updated with the latest information.

1. What are departing load charges? What projects must pay them?

In recent years, the most common application of departing load charges has been for direct access customers. Direct access is a program for large customers with industrial load or large campuses who procure energy from a third party. It’s like a CCA, but tailored to individual large customers.

The type of departing load charge that is assessed to non-export solar and storage is Customer Generation Departing Load. This is the portion of an IOU electric customer’s load that the customer serves with self-generation to replace the IOU. Reductions in load are classified as Customer Generation Departing Load only to the extent that such load is served with electricity from a source other than the IOU. For non-export systems, that is equal to the amount of generation, since all generation is used for onsite load when there is no export.

According to the tariffs, customers are required to notify the IOU at least 30 days in advance of reduction of electric service in the case of departing load. In practical terms it is processed as part of the interconnection application.

More details are in the departing load tariffs for PG&E, SCE, and SDG&E.

2. How much are these charges per kWh?

The overall departing load charge is an aggregation of multiple individual charges. These are the non-bypassable charges that people are familiar with in the NEM2 context.

Some of the charges vary slightly on different rate schedules. To find the exact amount of departing load charges, you need to look at the rate sheets for the specific rate the customer is on.

One controversial and significant non-bypassable charge is the Power Charge Indifference Adjustment (PCIA), which charges customers for the costs of energy contracts the utility has procured to serve you. This NBC does not apply to departing load. The Commission ruled in 2008 that Customer Generation Departing Load is exempt from departing load charges associated with the costs of utilities procuring new generation resources. The Commission reasoned that since utility forecasts already consider growth in customer generation, the utilities are actively procuring less generation due to customer generation.

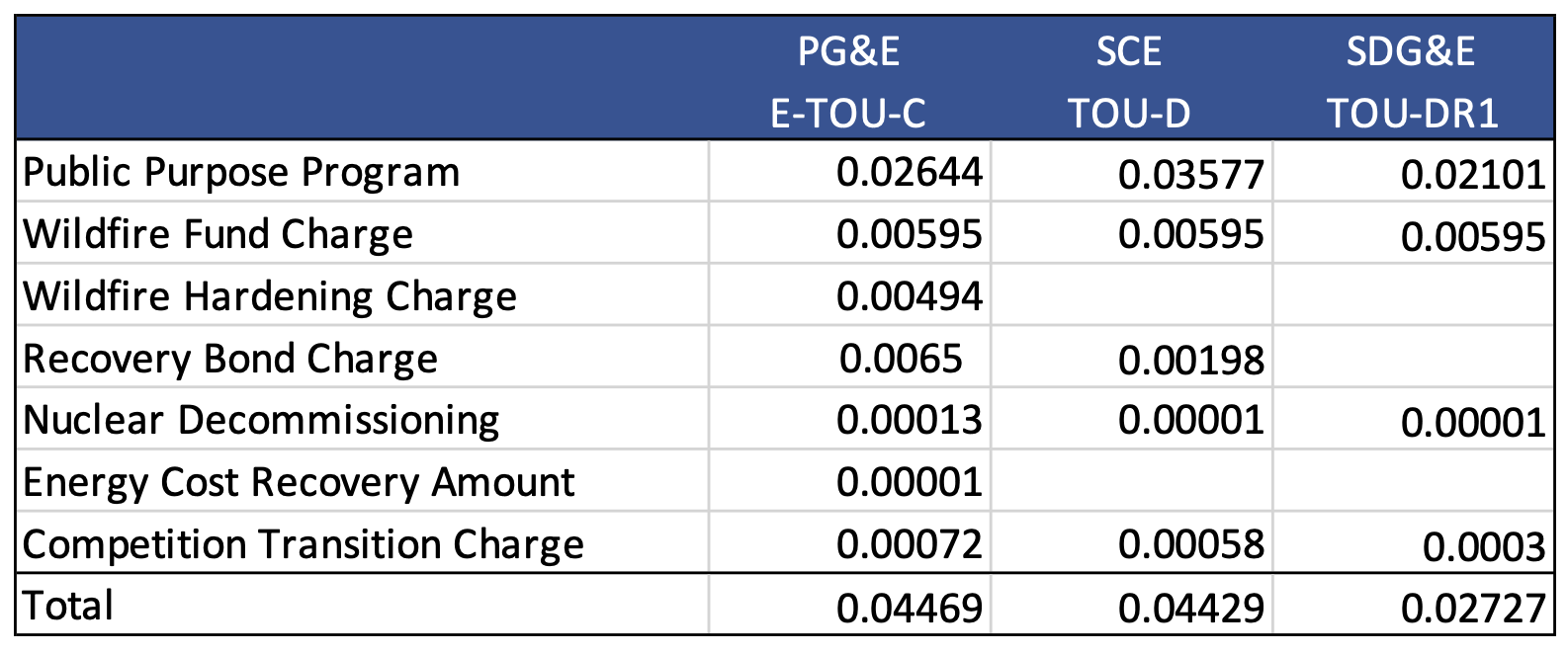

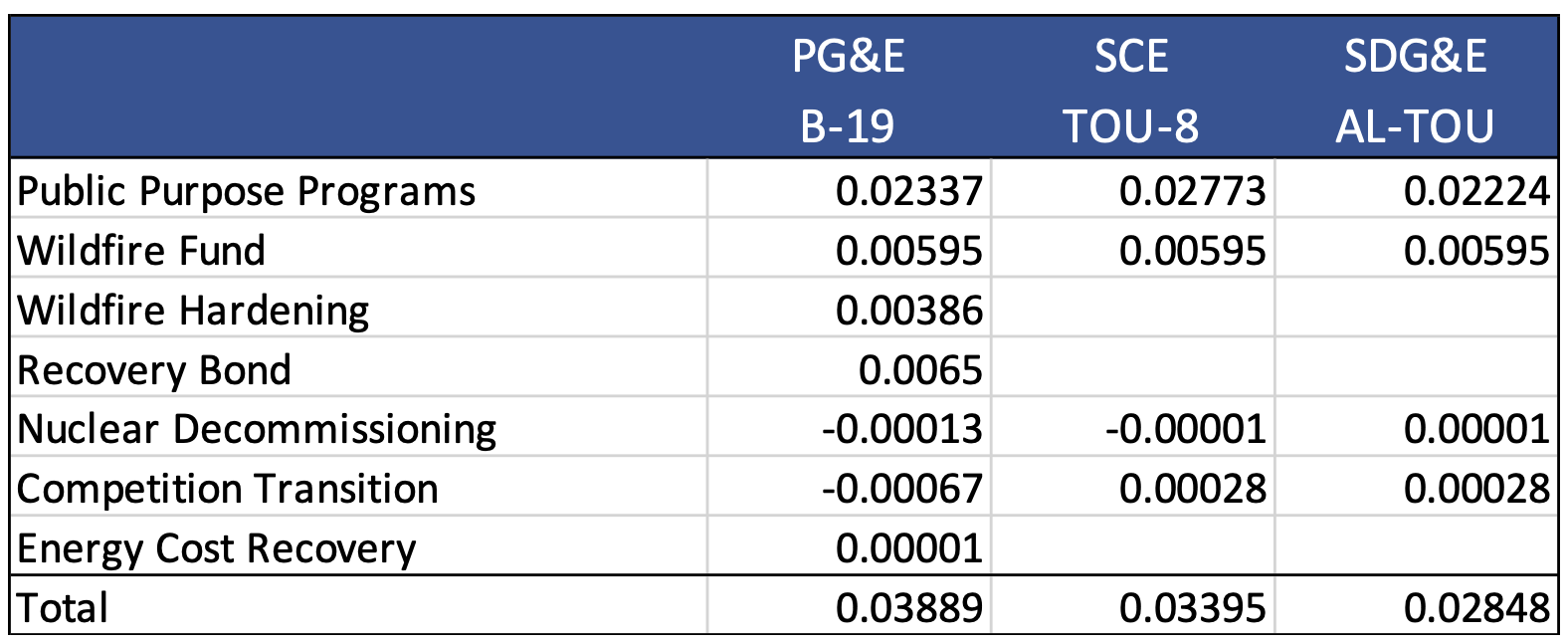

Below are the charges for default residential TOU rates and common commercial rates. For PG&E, there may be a credit to reduce the Recovery Bond Charge when funds are available. In the SCE rate schedules, the Recovery Bond Charge is called the Fixed Recovery Charge.

Departing Load Charge Amounts for Residential Default TOU Rates ($/kWh)

Departing Load Charge Amounts for Common Commercial Rates ($/kWh)

3. What are the different options for calculating the size of Customer Generation Departing Load?

PG&E

PG&E uses this form for selecting how to calculate departing load charges. It offers six different ways to calculate the charges. Options 1-3 calculate total customer load for cases where all load will be met with onsite generation. Options 4-5 estimate generator output. Option 6 is only for generation using the RES-BCT tariff. Option 5 is likely preferable if the customer’s added PV system is smaller than the customer’s historic usage.

Option 5 calculates departing load by estimating generator output using a capacity factor. The formula is Generator Size (kW) x Hours of Operation (24 x 30 = 720 hours monthly) x Capacity Factor = Monthly Departing Load. PG&E uses an 18% capacity factor, but they are open to using a more accurate capacity factor based on modeled solar output for an individual system. CALSSA is pressing PG&E to use 17.1% as the default.

As an example, a customer who installs a 6 kW non-export PV system has a calculated departing load for the month of 6 kW x 720 hours x 0.18 = 777.6 kWh. If the customer is on the residential E-TOU-C schedule in PG&E territory, the departing load rate is $0.04469/kWh per Table 2. For this customer, their total departing load charge for the month would be $0.04469/kWh x 777.6 kWh = $34.75.

Option 1 uses demand and energy usage over the past 12 months. Option 2 is similar, using the average 12 month demand and energy usage over the past 3 years. PG&E has confirmed that for Options 1 and 2, these options are based on historical consumption rather than production, and PG&E uses the 12-month historical usage prior to the submittal of the notice of departure and not the permission to operate date. However, PG&E does not subtract current metered usage from the historical metered usage to bill the monthly departing load charges. What will be billed monthly is the historical monthly consumption, using the 12-month historical usage prior to the submittal of the notice without any deductions for current usage.

Option 3 uses the average 12 month data based on the expected annual energy production for the generating facility as declared in the Generation Facility Interconnection Agreement. This is equivalent to using a 100% capacity factor. This would vastly overestimate departing load charges for solar.

Option 4 requires a net electric output meter that would provide actual usage based on future meter data. It is unclear how this exactly works. CALSSA understands this be an NGOM on the non-exporting generating system, but the utilities have not clarified.

Option 6 billing is for oversized generators participating in the Renewable Energy Self-Generation Bill Credit Transfer (Schedule RES-BCT) program, whereby the generating facility’s exports to the grid are used to offset charges for designated benefiting accounts.

SCE and SDG&E

SCE and SDG&E do not appear to have an option that is similar to PG&E’s Option 5. SCE and SDG&E offer options similar to Options 1, 2, and 4 from PG&E, meaning the only option that would accurately calculate departing load charges for solar would require an additional meter. CALSSA does not expect the utilities to actually implement departing load charges in this way. We are working with these two utilities to improve and clarify their options.

4. What exemptions are available?

If new load is fulfilled without using IOU-owned T&D facilities, it is exempt from nonbypassable charges. Thus, if a generating system powers loads that are isolated from the grid, departing load charges should not apply. Special Condition 6 of PG&E’s tariff states that “In accordance with Public Utilities Code Section 369, a new electric consumer, which locates in PG&E’s service area as it existed on December 20, 1995 (and any incremental load of an existing PG&E customer) shall be responsible for paying Nonbypassable Charges as applicable, except where such consumer's new or incremental load is being met through a direct transaction that does not make any use of transmission or distribution (T&D) facilities owned by PG&E.” The tariff gives PG&E the right to require a physical test that the new customer load can be islanded. The same is true for the other IOUs. A detailed explanation of this physical test can be found in SCE Preliminary Statement W, Section 4, Sheet 6.

Currently, none of the exemptions in Schedule E-DCG, Special Condition 2. (a – i) apply for solar generators. However, there are some exemptions from certain nonbypassable charges for those customers receiving discounts under the California Alternative Rates for Energy (CARE), Family Electric Rate Assistance (FERA), or Medical Baseline programs. Those exemptions are listed below and more information on these exemptions can be found in Schedule E-DCG under the RATES section for each of the non-bypassable charges.

California Alternative Rates for Energy (CARE) exemptions:

Wildfire Fund Charge, Wildfire Hardening Charge, Wildfire Hardening Fixed Recovery Charge Balancing Account, Recovery Bond Charge, Fixed Recovery Bond Balancing Account, and the Recovery Bond Credit

Family Electric Rate Assistance (FERA) exemptions:

Wildfire Hardening Fixed Recovery Charge Balancing Account, Recovery Bond Charge, Fixed Recovery Bond Balancing Account, and the Recovery Bond Credit

Medical Baseline exemptions:

Wildfire Fund Charge